The bread and butter of a traditional bank is the provision of loans. Although banks have reduced their dependency on this main source of income by branching out into other fields of the financial services world, the creation of loans is still a very important economic service. These loans are granted to households, business and to other banks, can be short or long term in nature, having a fixed, flexible or no interest rate and will be subject to different assurances such as collateral.

What is common between all loans is that they all carry a risk – the most basic of which is the risk that the loans become bad-debts or non-performing because the person or entity that took the loan can no longer service it. Non-performing loans will always be a problem for all banks since no model can ever cover all the risk involved and from time to time some borrowers will inevitably be faced with situations that were thought unlikely to happen.

From a regulatory point of view, a loan becomes a non-performing loan once more than 90 days elapse without the borrower paying the agreed instalments. Sometimes the banks can manage to agree new terms with such borrowers but at other times the bank would simply have to write off the loans and try to collect on the collateral and guarantees it would have secured before granting the loan. Banks also have the option of selling off the loans, but this will be at a discount and is dependent on finding someone to take on that debt.

What is the cost of non-performing loans?

It should be kept in mind that the cost of non-performing loans is a direct burden on the bank but an indirect burden on potential borrowers. As a bank is faced with more and more non-performing loans it would inevitably have to tighten credit and thus lend out less money. It must do this since its profits will start getting eaten away by the cost of managing the non-performing loans. Although loans are an asset for a bank they also come at a cost. The cost is not just the opportunity cost of using the same money for a different venture, but also the regulatory cost of keeping the loan on its books.

Therefore, as the number of non-performing loans rises the greater economy will suffer as loans become more expensive and less available. The expense could be in the form of higher interest rates, higher requirements for collateral and more stringent terms for the borrowers. As these factors come into play it would automatically become more difficult to obtain credit from a bank and thus some people and entities will be rejected for a loan. As credit becomes more difficult to obtain businesses will invest less and private individuals will take on less projects. So the effect on the whole economy is multiplied since less work is generated.

How do EU countries compare on Non-Performing Loans?

The below chart depicts the amount of non-performing loans as a percentage of total loans for the EU countries as at March 2016:

As expected the countries with the biggest economic problems have the highest percentage of non-performing loans. Countries like Cyprus which experienced a banking sector crises in 2012/13 and the so called PIIGS (Portugal, Ireland, Italy, Greece & Spain).

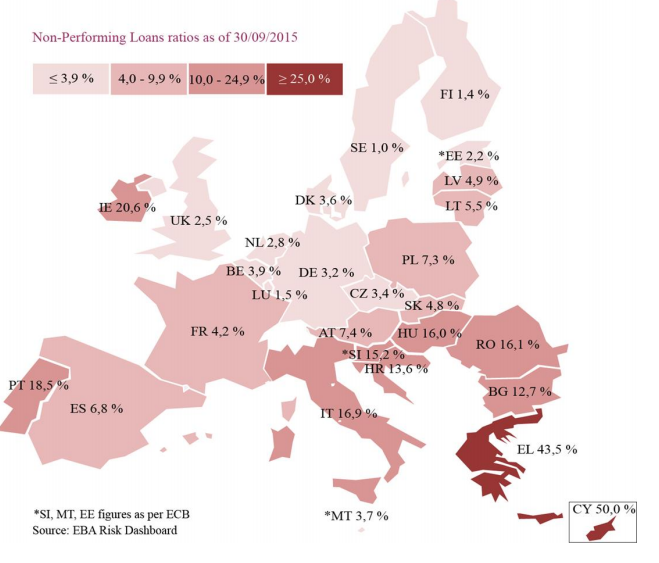

If we focus on the worst two countries (Greece and Cyprus) we can see that almost half the loans that have been issued are not being serviced. This of course is a very worrying situation for these two countries which is very difficult to get out of. These two countries are quite apart from the rest of the pack with the next worst country having a percentage of around 20%, which is still worrying. Ireland has started to improve as an economy but the percentage of non-performing loans is still quite high at around 15%. Having said that, the figure has gone down from the 20% registered in September 2015. Malta is sitting around mid-table, however it is worrying to see that over a period of 6 months the figure went up from 3.7% to 6.8%.

The below figure shows the same rates 6 months earlier as at September 2015:

The Bottom Line

Non-Performing loans are an indicator of economic health. The higher the percentage of such loans to total loans the more difficult and more expensive it is to obtain loans. This has a ripple effect on the economy as less investment and private consumption is registered. This is why the regulators place great emphasis on the measurement and management of these loans. Supervisors monitor the overall level of non-performing loans across euro area banks. They also check whether individual banks adequately manage the riskiness of their loans and if they have appropriate strategies, governance structures and processes in place. This is part of the common supervisory review and evaluation process (SREP) that is carried out for each significant bank every year. Furthermore, the European Central Bank regularly carries out coordinated exercises to review the asset quality of the banks it directly supervises.

KD

{kind=link}