It is no secret that for the local investor the preferred choice of asset class is normally the Fixed Income class. Fixed Income investments generally pay a fixed or quasi-fixed return on a regular, pre established basis. The assets class encompasses many different sub-categories such as:

- Direct Bonds – which make interest payments and repay the principal on a fixed schedule. Interest and principal payments are subject to the creditworthiness of the issuer.

- Bond Funds – invest primarily in individual bonds. Many make periodic dividend payments based on the interest paid by the bonds held in the fund.

- Fixed Income ETFs – Exchange-traded funds (ETFs) are baskets of investments that trade as a single unit throughout the day.

- Money Market Funds – are managed to help preserve your principal by investing in lower-risk debt securities with shorter maturities.

This post will focus mainly on the two most preferred genres of direct bonds and bond funds.

Direct Bonds

A bond is essentially a loan issued by a corporation (company) or a sovereign (government). The issuer of the bond will normally agree to pay a fixed or variable interest known as a coupon at fixed time intervals, for example annually or semi-annually. A bond will have a pre-determined maturity date at which point its face value will be paid which is normally the same price it would have been issued at.

Please refer to the below video for a quick visual explanation of the basic features of a bond:

Why would a company want to issue a bond rather than go to the bank? First of all there is the issue of cashflows required to service a bond as opposed to the cashflows required to service a bank loan. With a regular bank loan the company would have to pay interest plus capital on a regular basis, normally monthly. Granted there are interest only loans which will allow for a short period where only the interest payment needs to be made.

On the other hand, when issuing a regular bond it is only the annual or semi-annual interest payment that needs to be paid. If the company is successful and investors still want to remain invested in the company the bond issuer can simply roll over the bond at the end of the term and not have to pay the capital at all. This means that the issuer will issue another new bond to pay for the old bond.

In the years after the 2007-2009 financial crisis, on the local market we have seen many new bond issues, especially given the lower interest rates that prevailed. This has even caused a wave of roll-over issues especially on bonds that had a callable date and that were issued at a higher interest rate previously. a callable date is simply when a bond has more than one fixed date when it can mature. At the option of the issuer the bond may be matured (or called in) at an earlier date than the final maturity date.

Imagine it is 2005 and a company issued a bond at a rate of 7% maturing in 2012-19. Since in 2012 interest rates were much lower than they were in 2005 it would make perfect sense for the company to issue a new bond, say at an interest rate of 5% and use the proceeds to pay off the old bond. Considering that an average local corporate bond would be for around €30 million, that 2% saving in interest would result in a €600,000 annual cost saving.

One has to also keep in mind that not all bonds are the same. Every issuer has its own set of risks and generally speaking

“The higher the interest rate offered, the higher the risk involved.”

Even the same issuer can have different ranking bonds ranging from senior, secured, un-subordinated to junior, unsecured, subordinated. These terms are all referring to the ranking of the bond in the event of a default of the issuer. One must also keep in mind that a senior bond of one issuer is not necessarily less risky than a subordinated bond of another issuer. For example, what would you consider more risky: a subordinated bond of a well established bank which is highly regulated and has a strong capital base, or a senior bond which is issued by a small company that operates in the IT sector?

Bond Funds

Bond Funds are basically portfolios of direct bonds put together. So when you own units in a bond fund you are essentially owning part of a portfolio of many different bonds. Bonds held within the fund portfolio are designed to mature on a staggered basis so that income payments are delivered consistently.

A bond fund would have a fund manager who will be responsible to take the investment decisions within the fund. The fund manager replaces bonds as they mature, when the issuer’s credit is downgraded and when the issuer “calls,” or pays off the bond before the maturity date. The fund manager could even have profit targets at which point they would sell a holding. Alternatively bonds could be sold since the outlook of the issuer is no longer favourable.

Some bond funds are designed to mimic the broader market, while others specialize in high-yield (riskier) bonds, short-term debt, emerging markets or governments bonds. Some focus on certain geographical locations or issuing currency of the bonds.

Bond funds typically pay out interest payments on a regular basis which is normally monthly or quarterly. The income paid would be coming from the income earned by the fund. A major difference between a bond fund and a direct bond is that a bond fund does not have a maturity value at which point the capital would be returned as in the case of a direct bond.

Risks associated with Bonds & Bond Funds

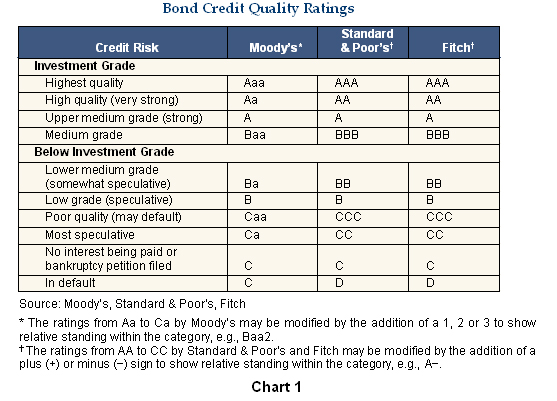

A way to gauge the risk of a bond that has been used for many years is to look at the bond’s credit rating. Credit rating agencies like Standard and Poors, Fitch and Moodys are in the business of assessing a company to determine how risky it is as an issuer. They then use their own credit rating scores to determine the riskiness they perceive vis-a-vis that issuer.

The below table gives a detailed definition of the different ratings:

Of course credit ratings are just covering one type of risk involved in investing into bonds which is defined as default risk. This refers to the risk of the issuer defaulting on payments and being forced to restructure or file for bankruptcy. There are other risks involved with investing into bonds which include:

- Interest Rate Risk – Interest rates and bond prices have an inverse relationship; as interest rates fall, the price of bonds trading on the market normally rises. On the other hand, when interest rates are rising, the price of bonds tends to fall. This happens because when interest rates are on the decline, investors try to capture or lock in the highest rates they can for as long as they can. To do this, they will buy into existing bonds which have a relatively higher interest rate than the prevailing market rate. This increase in demand results into an increase in bond prices. Conversely, if the prevailing interest rate were on the rise, investors would naturally try to sell their existing bonds that now would be paying a relatively lower interest rates. This would force bond prices down.

- Reinvestment Risk – the risk of having to reinvest proceeds at a lower rate than the funds were previously earning. Many investors have experienced this over the last 5 years or so when interest rates fell over time and callable bonds were exercised by the issuers. Active bond investors can attempt to mitigate reinvestment risk in their portfolios by investing into bonds with different maturity/call dates. This limits the chance that many bonds will mature or be called at once.

- Inflation Risk – this occurs when the cost of living (or inflation rate) erodes the real return that an investor earns. This risk is quite present at the moment. If an investor buys a bond that pays a fixed 1.5% interest but the inflation rate is at 2% then the real return is -0.5%.

- Liquidity Risk – this is the risk of not being able to sell your bond. Government bonds are generally easier to trade, but corporate bonds, especially in times of panic could be quite difficult to trade.

The Bottom Line

So considering all the above, which is better to invest into at the moment, bonds or bond funds? Like many cases in finance it all depends and a combination of the both is most likely the ideal option.

Bond funds have the advantage that they offer a diversified portfolio at a much smaller capital investment than if one had to make up a similar portfolio on their own. So for an investment of say €5,000 you can invest into a bond fund that would be invested into 200 different bonds for example. A bond fund will be managed by the fund manager who would be active in balancing the portfolio in order to take advantage of market situations and hedge against potential adverse movements. This might be difficult to do with a portfolio of direct bonds since the investor might not have the time or expertise to do so.

An advantage of direct bonds is that they have a maturity date at which time (excluding default of the issuer) the face value of the bond would be paid. With a bond fund, it is like holding a perpetual investment with no end date. However the bonds within the fund will have a maturity date and the duration of the fund is an important feature to note when choosing a bond fund. In simple terms a bond’s duration is the amount of time in years it would take to get back the investment made to buy that bond.

What about the cost? Generally speaking bonds are cheaper to buy. An international bond will normally cost around 1% whereas local bonds are even cheaper to trade. With a bond fund they normally have around 3-5% as an upfront fee and an annual management fee of around 1% that is taken form the fund. Why do bond funds have such higher costs? Essentially it is the same reason why bond funds can be a better choice – cost of the fund manager, their teams in charge of research and sales and also the charges of the broker have to be recuperated through these fees. Like with many things in life, nothing of good quality comes free in the world of finance.

Taking a more practical view now, in the current situation where we have

- very low interest rates,

- prospects of interest rate increases possibly from next year (keep in mind that as interest rates rise the prices of existing bonds normally falls),

- low liquidity in the market to buy direct bonds (investors that hold existing bonds are reluctant to sell them knowing that yields have fallen).

What should an investor opt for? If the investor is looking for regular income (example monthly or quarterly), looking for a diversified portfolio to spread his/her risk among different issuers and wants to get a full allocation of the money he/she wishes to invest immediately, then based on the above a bond fund is looking most attractive for such an investor. It is however important to note that not all bond funds are the same. One has to look for large bond funds with a decent spread of different bonds and a health level of cash balances. It is also important to have a bond fund with a track record to see how the fund performed in normal, difficult and good times. Another important feature is the duration of the bonds within the fund. Given the current interest rate scenario it is important to stick to bond funds with short durations, say 3-4 years since these will face lower risk when interest rates do increase. Finally it is important to check which are issuers the bond fund is investing into. This can easily be found on the annual accounts of the fund and the top 10 holdings of the bond fund are normally found on the fund’s fact sheet.

So should direct bonds be disregarded, not quite. Unfortunately on the local market new bond issues are being so over subscribed that an investor wanting to invest €10,000 is normally being left with around €1,500 to €2,000 allocation and receiving the difference back as a refund. This is not an issue with bond funds since the exact amount desired is normally easily purchased or sold within a few business days. Direct bonds can also be bought on the market (i.e. buy buying existing bonds). Granted, the prices of existing bonds are quite high at the moment, however one has to consider the yield the bond is paying and not just the price one is paying for it. So when considering the “high” price of the bond and the coupon it is paying, is the yield still attractive?

What about Malta Government Stocks (MGSs)? There is still some money to be made here, but I will focus on this topic in a whole separate post dedicated to MGSs.

For more info on this or any other finance related topic, please do not hesitate to contact me on kd@financebykd.com or by using the Contact KD form on the site.

KD

Copyright secured by Digiprove © 2015

Copyright secured by Digiprove © 2015